What City and METRO decision makers need to understand: It makes far more sense for our cities and region to fund large long-term infrastructure with Low Cost Government Bonds instead of skyrocketing Development Cost Charges (DCCs) on new housing.

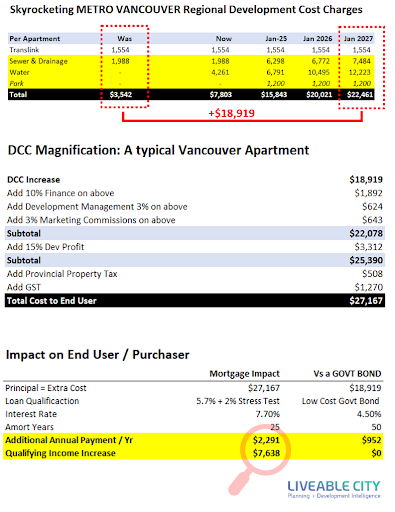

Most people don’t appreciate that DCCs get magnified when added to a development budget and they are far more damaging to end users. As an example, the table below shows METRO’s proposal for a more than six-fold increase in Regional DCCs on Apartment construction in Vancouver. These additional fees must be financed and managed when they get added to the cost of a new apartment. They raise the bar on the amount of profit a homebuilder has to earn in order to satisfy the 15% return on cost required by banks before they approve finance for new construction. And because DCCs (+Finance +Development Management + Marketing + Profit) get added to the end price of the apartment, these costs are again magnified by the 2% Provincial Property Transfer Tax, and the 5% Federal Goods and Service Tax when a purchaser takes possession of a new home.

What’s the impact on the purchaser? The $18,919 DCC increase shown grows to $25,390 after financing and additional development costs. And after Federal and Provincial taxes, the added cost grows to $27,167 which gets tacked on to someone’s new mortgage! Higher mortgage payments put home ownership further out of reach, increasing the annual income needed to qualify for a mortgage by more than $7,500.

Some people suggest that ‘new housing should bear the brunt of the cost of new infrastructure’ [not equitable]; ‘existing homeowners have paid their share already’ [untrue]; and ‘the cost of the DCC will just come out of the land price paid by the developer’ [myth] and won’t impact the end price of homes [also a myth].

The far more sensible alternative is to raise a low-cost government bond at lower interest and a longer amortization period to finance long-term infrastructure upgrades. It is nonsensical to foist these costs onto new mortgages for new housing at higher interest rates and shorter amortization periods. The bond alternative shown could be financed at less than half of the cost of the DCC increases proposed by METRO. The Feds, Province, Region and City should instead partner on major growth-and-climate-change driven infrastructure upgrades in Canada’s urban centres and finance the same with low cost bonds underwritten by all taxpayers.